How Public Markets Already Own the AI Frontier

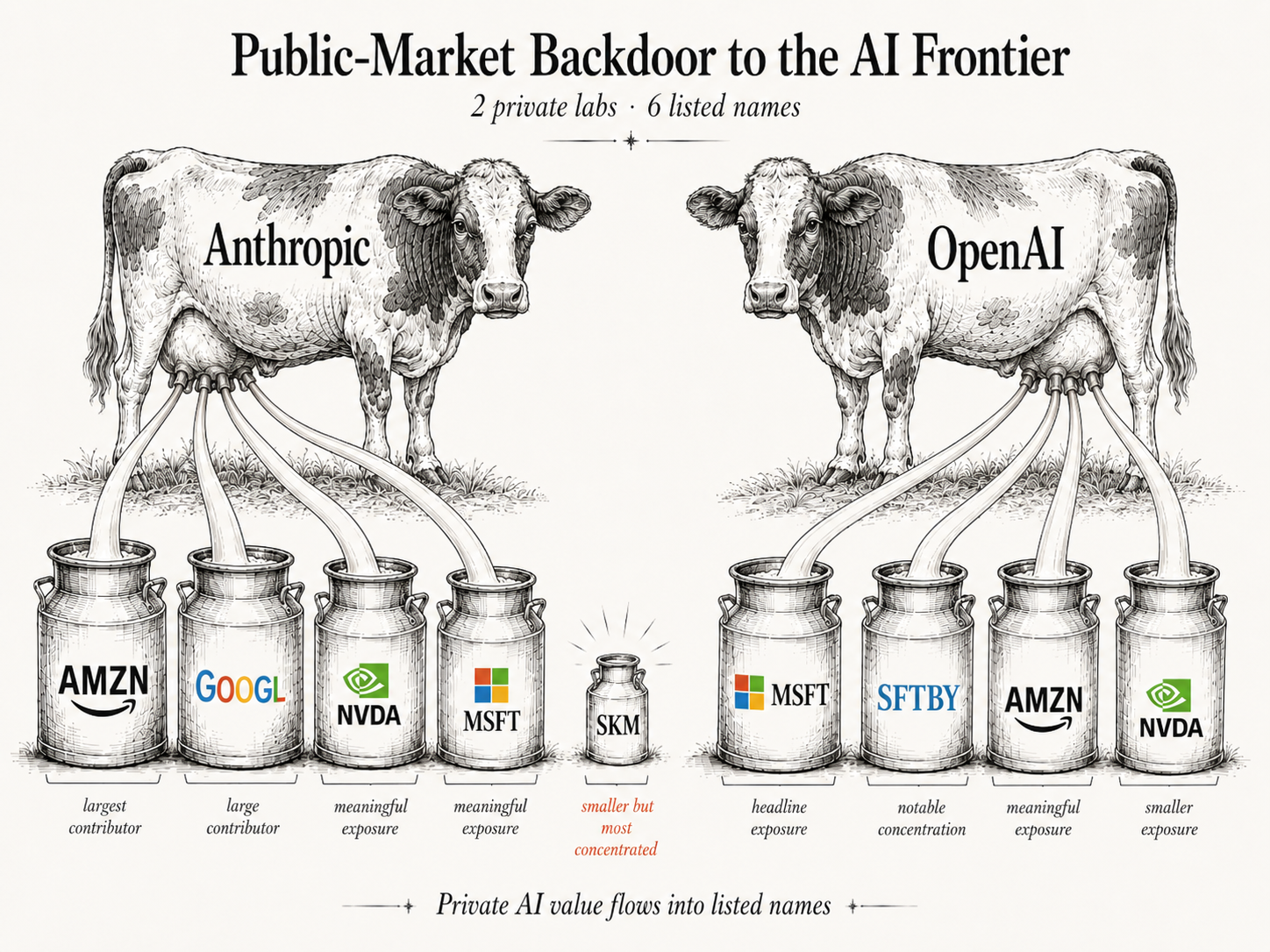

Public-market exposure to Anthropic and OpenAI spreads across six listed names. The AI-lab share of each parent's market cap ranges from under 1% to over 40% — and the most concentrated bets aren't the ones most investors reach for.

Synopticon · April 30, 2026 · Reference valuations: OpenAI $852B (post-money, April 1), Anthropic $900B (rumored Q2 round)

If you wanted to buy Anthropic or OpenAI through a public stock, what would you pick? Most people say MSFT or NVDA. The actual answer — if "concentration of stake relative to market cap" is what you mean by an AI-lab bet — is two foreign-listed names: SoftBank Group (SFTBY, ADR for 9984.T) and SK Telecom (SKM, ADR for 017670.KS).

This piece walks through who actually owns Anthropic and OpenAI on the public side, why the dollar headline numbers are misleading, and how the accounting fictions, NAV discounts, and friction costs sort the six listed names into very different kinds of trades.

Concentration, not dollars

Six US-listed companies hold meaningful stakes in the two frontier labs. Ranked by share of the parent's own market cap that is the AI-lab stake, they look like this:

| Ticker | Lab | % of market cap | Implied stake (USD) | What it really is |

|---|---|---|---|---|

| SFTBY | OpenAI | ~44% | ~$94B (11% of $852B) | Largest external private investor; held inside a holding company at a NAV discount |

| SKM | Anthropic | ~17% | ~$2.4B (0.27% of $900B) | Diluted from 2% in 2023; smallest stake, largest concentration |

| MSFT | OpenAI + Anthropic | ~7.9% | ~$240B aggregate | Equity-method accounting on OpenAI; carrying value $135B, not the $230B fair value |

| AMZN | OpenAI + Anthropic | ~7.0% | ~$200B aggregate | Anthropic mostly markup; OpenAI $50B is $15B firm + $35B contingent |

| GOOGL | Anthropic | ~2.6% | ~$110B | Capped at 15% of Anthropic by DOJ antitrust agreement |

| NVDA | OpenAI + Anthropic | ~1.0% | ~$50B aggregate | Mix of equity and compute-credit consideration; split undisclosed |

Market caps as of April 30, 2026: MSFT $3.03T · AMZN $2.85T · GOOGL $4.20T · NVDA $4.85T · SFTBY $213B · SKM $14.3B.

The spread between the most and least concentrated public bet is roughly 50×. That's the article.

Anthropic's public shareholders

- Amazon (~$150B, 16.5%) — the largest external holder. Cash invested is closer to ~$8B; the rest is unrealised markup as Anthropic's round-over-round valuation climbed. Amazon and Google both have AWS/GCP commitments tied to the equity.

- Alphabet (~$110B, 12.5%) — mirror pattern: ~$3B in cash since 2022, the rest is markup. The stake is capped at 15% by a DOJ antitrust agreement, so Alphabet can't lean further in even as new rounds come around.

- Nvidia (~$20B, 2.2%) — small dollars, strategic position. Compute-credit linked, not cash-only.

- Microsoft (~$10B, 1.1%) — from a 2025 strategic investment alongside the AWS/Anthropic deployment expansion. Booked at cost under the equity method (Microsoft owns <20% of Anthropic, so this one isn't equity-method on its own).

- SK Telecom (~$2.4B, 0.27%) — the structural anomaly. The smallest stake on the chart, but ~17% of SKM's own $14.3B market cap. The position has been diluted from an initial ~2% (2023, when Anthropic was at $5B) down to 0.27% today — while the lab valuation rose ~180×. The cost basis is among the cheapest entries on the cap table.

OpenAI's public shareholders

- Microsoft (~$230B fair value, ~$135B carried, 27%) — the marquee number is theoretical, not booked. After the October 2025 PBC restructuring, Microsoft uses equity-method accounting and carries the stake at ~$135B. The April 2026 $852B round did not generate a markup on Microsoft's books.

- SoftBank Group (~$94B, 11%) — the largest external private investor by both stake and cash committed. This is the position that makes SFTBY's market cap 44% OpenAI.

- Amazon (~$50B, 5.9%) — $15B is firm equity; $35B is contingent on IPO and/or AGI milestones. Capital-call mechanics matter for present value.

- Nvidia (~$30B, 3.5%) — equity vs. compute-credit split is undisclosed. Some portion of the headline number is paid in compute rather than paid for.

- OpenAI Foundation (26%) and employees + early investors (26.6%) retain control. ~$3B of the $122B raised in the April round came from retail investors through secondary platforms — small as a percentage, meaningful as a sentiment indicator.

The accounting story

The same dollar of AI-lab equity gets treated radically differently across companies. This is the most underappreciated angle in any public-markets read of the sector.

Mark-to-market (Amazon, Alphabet). Both hold their Anthropic stakes at fair value. When a new round prices Anthropic up, the existing stake is marked up, and the gain flows through GAAP earnings. In Q1 2026, Amazon booked a $16.8B pre-tax gain on its Anthropic line. Alphabet booked $36.9B in equity gains (~$28.7B reaching net income), the bulk of it Anthropic-linked. If the rumored $900B Anthropic round closes in Q2, both could see another $50–90B in markups.

Roughly half of Alphabet's record $62.6B Q1 profit didn't come from search ads, cloud, or any product — it came from updating equity values, primarily Anthropic. More than half of Amazon's pre-tax income in the quarter was the same line item.

Equity method (Microsoft). A >20% stake forces equity-method accounting. Microsoft books OpenAI's actual losses and gains, not valuation step-ups. The carrying value is ~$135B, set at the October 2025 PBC restructuring. Through FY26: a $3.1B loss in Q1, a $7.6B gain in Q2 (the restructuring step-up), a $14M loss in Q3. The April 2026 $852B round generated no markup on Microsoft's books, even as the implied fair value of the stake jumped to ~$230B.

The circular-financing observation. When Amazon and Alphabet invest more in Anthropic, that activity helps push the next round price higher, which marks up their existing stake, which prints as profit. The accounting is technically correct. But the largest investors are materially influencing the valuations driving their own reported earnings. This is a unique feature of the current AI cycle — not present in any prior tech bubble — and it's worth flagging before any reading of the income statements.

SoftBank as the OpenAI proxy

SoftBank Group (SFTBY, the ADR for Tokyo-listed 9984.T) is a holding company. It is not SoftBank Corp. (9434.T), the Japanese telecom subsidiary — a confusion that costs unprepared retail investors more than it should.

SFTBY's gross NAV at end-April 2026 is roughly $343–381B: Arm Holdings (~$126B, public, 90% ownership), OpenAI (~$77–94B), the SoftBank Corp. telecom stake (~$26B), ByteDance (~$16–18B), Coupang (~$17B), PayPay (~$12–15B), other Vision Fund public positions (~$13B), the T-Mobile / Deutsche Telekom residual (~$10B), private AI bets (~$4–5B), and ~$25B of cash. After ~$90B of net debt, net NAV lands at ~$253–291B. The market cap is ~$213B. That gap is the NAV discount — ~25–30%, currently at the lower end of SFTBY's historical 20–60% range.

The discount exists for real reasons: tax leakage on realised gains, capital-allocation track record (WeWork, Wirecard, Katerra), illiquidity of private holdings, conglomerate management overhead, and ADR / currency mechanics. None of these are going away.

What's useful is the "two springs" mental model. SFTBY's stock moves on two independent forces:

- Underlying NAV growth (Arm rises, OpenAI rises, ByteDance rises);

- Discount compression or widening (sentiment, catalysts, AI cycle posture).

These can pull together (the 2024–2026 AI rally) or against each other (2022, when NAV fell and the discount widened — SFTBY dropped 60%+ in a year). For the investor whose thesis is OpenAI, the SFTBY trade is OpenAI exposure plus a sentiment bet on the discount, packaged together. That's not a bug; it's the trade.

SK Telecom: the asymmetric sleeper

SK Telecom is a Korean telco. Its core business is wireless service, fixed-line, and 5G infrastructure. Sitting on the balance sheet is a 0.27% stake in Anthropic, originally acquired in 2023 when Anthropic was valued at $5B. That ~$10M cost basis (rough estimate) has compounded against a 180× rise in the lab's valuation. At the rumored $900B mark, the position is worth ~$2.4B — about 17% of SKM's $14.3B market cap.

Two structural points:

- Cheap entry, no rerate. SKM trades on telco multiples. The market doesn't price the Anthropic stake at fair value the way it would for a tech holding company. An IPO catalyst — or even a clean secondary mark above $900B — would force a rerate.

- The smallest stake is the most concentrated bet. SKM owns the least Anthropic of any name on the chart. It also has by far the highest stake-to-market-cap ratio. The math works precisely because SKM is small.

The friction: SKM is a dividend-paying foreign telco with regulatory exposure (KCC), Korean tax treatment, and ADR conversion mechanics. It's not a clean Anthropic ETF.

Why direct secondaries aren't the answer

For accredited investors, Hiive, Forge, and EquityZen sell direct OpenAI and Anthropic shares. The pitch is "purity": skip the conglomerate friction, own the lab directly. The math doesn't quite hold.

- 40–70% premium to the last primary round price for OpenAI; thinner spreads for Anthropic but still 20–40% above the most recent funded mark.

- Platform fees of 3–5%.

- SPV fees of ~2%/year management plus 20% carried interest on gains.

- $50–250K minimums; accreditation required.

- Illiquid: ROFR clauses, no public exit, lockups around any IPO.

- K-1 tax forms, not 1099s. State filings multiply.

- No information rights. Common stock; subordinated to preferred liquidation prefs.

Stack the friction up and you lose roughly 25–40% of the theoretical purity gain to fees and taxes. A 3× gross return scenario nets ~2.3× through a typical SPV structure. For most accredited investors with sub-million-dollar checks, the public alternatives compete or beat that on a risk-adjusted basis — especially once liquidity is priced in.

The reframe

"AI exposure" through public markets isn't one trade. It's a small set of trades with very different shapes:

- MSFT, AMZN, GOOGL, NVDA are quality businesses with AI optionality. The AI-lab line is 1–8% of market cap. These names will track AI sentiment and earnings, but moves in the underlying lab valuation are diluted heavily by the rest of the parent's book. They're not bets on Anthropic or OpenAI — they're Big Tech longs.

- SFTBY is the cleanest concentrated bet for a retail-accessible investor. ~30% of NAV is OpenAI; the rest (Arm, Coupang, ByteDance, telecom) is mostly liquid or public. The trade comes with the discount and the holding-company risk priced in.

- SKM is the most asymmetric: smallest stake, largest concentration, cheapest cost basis, lowest market expectations. It's also the smallest-cap and least liquid. A clean Anthropic IPO or secondary above the current mark forces a rerate.

- Direct secondaries are for accredited investors with large enough checks ($1M+) to absorb SPV friction. For everyone else, the friction tax matches or exceeds the purity benefit.

The honest conclusion: there is no clean public AI-lab trade. The best risk-adjusted version is SFTBY at the current discount; the most asymmetric is SKM; the cleanest narrative trade is MSFT but the exposure is too diluted to count. Pick the trade-off knowingly.

Caveats & methodology

- Cap table numbers are estimates from public disclosures, Q1 2026 earnings, and reporting. Private cap tables are not fully transparent; figures should be read as approximate and round.

- Tax leakage reduces look-through value by 15–25% for corporate holders, depending on holding entity and jurisdiction.

- Microsoft's $230B is theoretical fair value; the balance-sheet carrying value under equity-method accounting is ~$135B.

- Amazon's $50B OpenAI is mostly contingent ($35B tied to IPO and/or AGI milestones).

- Anthropic's $900B mark is rumored from reporting on the pending Q2 round; the closed mark could land anywhere from $800B to $1T+.

- ADR mechanics apply to SKM (017670.KS) and SFTBY (9984.T): the look-through dollar exposure of the underlying entity does not pass through 1:1 to the ADR holder, and currency moves add noise.

- SoftBank Group (SFTBY) is the holding company. It is not SoftBank Corp. (9434.T), the listed Japanese telecom subsidiary — a frequent confusion.

- Anthropic restructured to a Public Benefit Corporation, which constrains pure shareholder primacy at the entity level.

- Liquidation preferences are not reflected in headline stake values. Anti-dilution provisions vary by holder.

- Secondary market pricing is thin and may not reflect the value of an institutional-scale block.